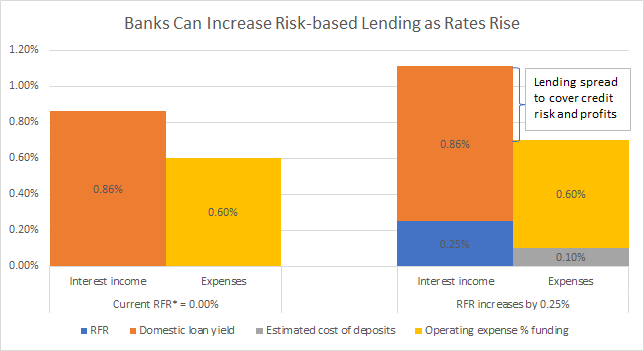

Higher yen interest rates will encourage Japanese banks to increase risk-based lending because they can allocate a growing proportion of their lending spreads to cover credit risk. With the short-term risk-free interest rates (RFR) and cost of deposits at close to zero percent currently, the majority of the banks’ 0.86% domestic loan spread goes to cover operating expenses, leaving only 0.26% of the loan spread to cover credit risk and for profits in the fiscal year ended March 31, 2023 (Exhibit 1) based on a rough calculation using data from the Japanese Bankers Association. Suppose, for example, RFR rises by 0.25 percentage points, the interest rate on deposits goes up by 0.1 percentage points, and the loan spreads remain unchanged. In that case, banks will earn 0.15% more risk-free interest income on deposits that partially offset operating expenses and free up lending spreads to cover additional credit risk and profits.

Exhibit 1:

* The average Tokyo OverNight Average rate was -0.03% in the fiscal year ended March 2023, but used 0.00% for illustrative purposes.

Source: Japanese Bankers Association

Some fear higher interest rates will dampen loan demand and thwart Japan’s fragile economic recovery. However, lending rates to credit-worthy borrowers are unlikely to rise as fast as market rates because banks can tighten loan spreads, as risk-free interest income offsets a growing proportion of their operating expenses.

Net interest margins on deposits will widen when RFR rises because deposit rates typically rise slower than market rates, particularly for banks with solid deposit franchises.

The banks’ operating expenses will continue to decline as they cut costs through digitization and branch closures, which will offset the upward pressure on the percentage of operating expenses to funding caused by the monetary tightening, which will shrink the denominator.