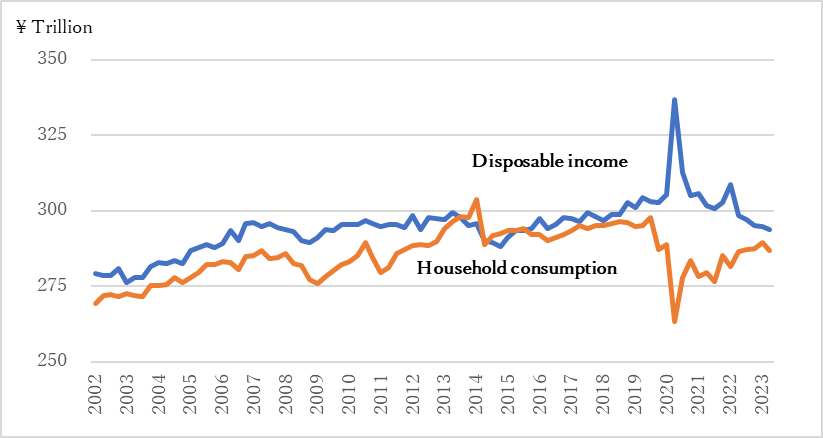

Anemic disposable income growth constrains household consumption and Japan’s economy (Exhibit 1). Signs of nominal wage growth are encouraging, but the raises in 2024 need to be bigger and more broad-based than in 2023 to boost real disposable income and consumption to positively impact real GDP and allow the government to reduce fiscal spending.

Exhibit 1: Anemic disposable income growth constrains household consumption.

Source: Cabinet Office

Japan’s economy will continue to struggle as long as discretionary income growth remains stagnant. In the quarter ending September 2023, household consumption accounted for approximately 52% of Japan’s real GDP.

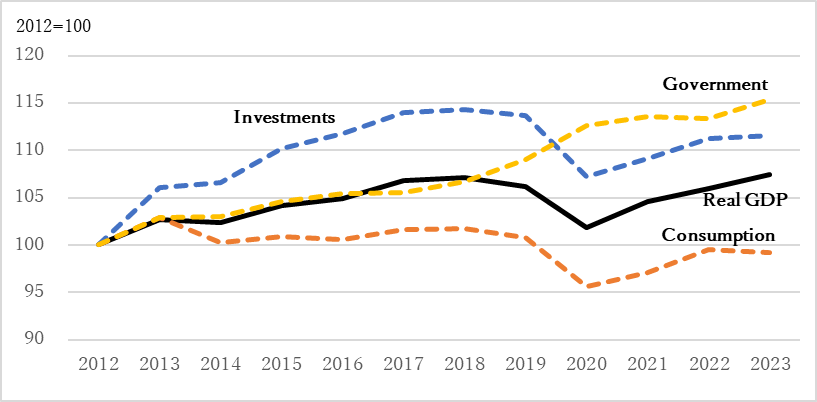

Japan’s economy, measured in terms of real GDP, has grown by 0.69% per annum cumulatively since 2012, while consumption has shrunk by 0.08% per annum. At the same time, investments grew by 1.05% per annum, supported by ultra-low interest rates, and government spending increased by 1.37% per annum (Exhibit 2).

Exhibit 2: Weak consumption weighs down overall economic growth

Source: Cabinet Office

Wages need to rise much faster than inflation to boost consumption

Disposable income will rise slower than gross salary due to bracket creeping because income deductions and tax brackets do not automatically adjust for inflation. Consumption will grow more gradually than disposable income because households in their prime earning years typically save a large percentage of incremental disposable income growth for home purchases, children’s education, and retirement. In addition, households are accumulating cash to pay down their housing loan outstandings when interest rates start to rise, as most housing loans in Japan have floating or fixed-to-floating interest rates.

Social benefit recipients tend to spend a more significant percentage of their disposable income, but consumption growth will lag inflation because benefits are structured to increase slower than inflation[1]. Social benefits accounted for approximately 19% of gross household income in 2022.

[1] https://www.mhlw.go.jp/english/wp/wp-hw3/dl/11-04.pdf.

About Rating Stretegy Institute